On January 11, 2023, the 103rd General Assembly was seated. It will run for two years until the next General Assembly is seated in January 2025. This General Assembly has 59 Senators (40 Democratic, 19 Republican) and 118 Representatives (78 Democratic, 39 Republican).

This is the first “normal” session since 2019. The sessions in 2020 and 2021 were altered by COVID-19 mitigations, and the timing of the 2022 session was revised and compressed due to the change in the date of the primary election from March to June. And this session also has a new House Speaker, House Minority Leader, Senate President, and Senate Minority Leader since the last “normal” session.

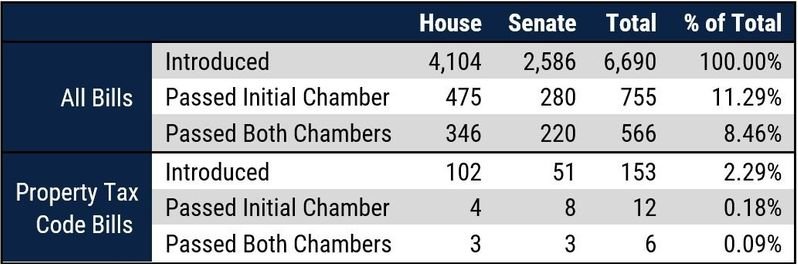

Together, the two chambers of the General Assembly considered nearly 6,700 bills before adjourning on May 27, including 153 proposed revisions to the Property Tax Code. By the end of the session, the General Assembly adopted fewer than 9% of all legislation introduced, and fewer than 4% of legislation related to property taxation.

Of the 153 bills that were introduced regarding the Property Tax Code, the largest share (41) were designed to expand eligibility or benefits relating to homestead exemptions. Sixteen of these targeted the expansion of the Low Income Senior Citizen Assessment Freeze Homestead Exemption. In the end, only HB 2507 (described below) passed. No changes were made to any other exemptions.

Proposals to create a Mega Projects classification (HB 3565 and SB 1350) designed to incentivize the Chicago Bears’ move to Arlington Heights were introduced, but neither was heard in committee.

By the end of the session, only six bills amending the Property Tax Code had passed. While this is less than one-tenth of 1% of all the legislation that was introduced, changes to the Property Tax Code often have a greater impact than such numbers would suggest. The six bills that passed include:

- HB 2289 is a General Revisory bill, which is needed whenever two public acts address the same section of a statute in the same year; such a bill merges them into a single statute for future years. This bill makes no substantive changes, and it takes effect upon becoming law.

- HB 2507 can best be described as an omnibus bill, which addressed a variety of concerns related to the Property Tax Code and placed them into a single enactment. Its provisions include:

- Adding a 100% property tax exemption for Veterans of WWII to the Standard Homestead Exemption for Veterans with Disabilities (SHEVD), effective for the 2023 (payable 2024) tax year;

- Revising the SHEVD to make homes with assessed values of $250,000 ($750,000 fair cash value) eligible for an exemption of $250,000, effective for the 2024 (payable 2025) tax year;

- Eliminating the requirement of an honorable discharge for the SHEVD, effective for the 2024 (payable 2025) tax year;

- Creating a new 50% exemption to surviving spouses of first responders, effective for the 2024 (payable 2025) tax year;

- Creating a preferential assessment procedure for non-profit Regional Wastewater Treatment Facilities, effective for the 2024 (payable 2025) tax year.

- Excluding property tax extensions made by park districts for aquarium and museum purposes from being subject to the Property Tax Extension Limitation Law (PTELL), effective immediately;

- Creates a new maximum tax rate for park districts for aquarium and museum purposes, effective immediately;

- Provides a new referendum method for increasing a tax levy under PTELL, effective immediately;

- Providing that Townships with populations between 1,000 and 2,999 residents (currently, fewer than 1,000 residents) must be grouped into a Multi-Township Assessment District and elect a single Assessor, effective with the first election after the 2030 decennial census;

- Creating a new ten-year homestead exemption for single-family homes built by a municipality on exempt municipal-owned land that was then sold to owner occupants (subject to County Board approval in all counties with fewer than 3,000,000 residents), effective for the 2024 (payable 2025) tax year.

- Requiring Cook County to value nursing homes and residential mental health facilities in the same classification as residential properties, effective immediately.

- HB 2539 provides that compensation paid to County and Township officials by the Illinois Department of Revenue will instead be provided directly to the Township and County governments, who will then issue the compensation to the local officials; this act takes effect upon becoming law.

- SB 74 creates the Property Tax Payment Plan Task Force, which will investigate developing a system designed to prevent eligible tax-delinquent owner-occupied properties in Cook county from being sold at the annual tax sale. A report detailing the Task Force's findings, conclusions, and recommendations shall be submitted to the General Assembly no later than November 15, 2023. The Task Force is dissolved upon submission of the report.

- SB 1225 permits chief county assessment officers in all counties to require an application for the preferential assessment for subdivision common area; currently, only Cook County may do so. This act takes effect upon becoming law.

- SB 1675 is a far-reaching bill designed to reform the tax sale system in Cook County by a variety of measures, including:

- Preventing a small number of tax buyer from exploiting loopholes in the system;

- Permitting local governments to take control of blighted properties and targeting them for redevelopment; and

- Lowering the monthly interest rate charged for delinquent Cook County taxes from 1.5% to 0.75% per month.

This act takes effect upon becoming law.

Each of these bills still needs the Governor’s signature before becoming law. For more information, the text of the legislation can be viewed on the General Assembly’s web site at www.ilga.gov.

Mark D. Armstrong, CIAO-M, is the Supervisor of Assessment for Kane County; he chairs the Legislative Committee of the Illinois Association of County Officials and has drafted part or all of more than a dozen pieces of legislation that are now part of the Illinois Property Tax Code.